Student borrowers can learn more about preparing for payments at studentaid.gov.

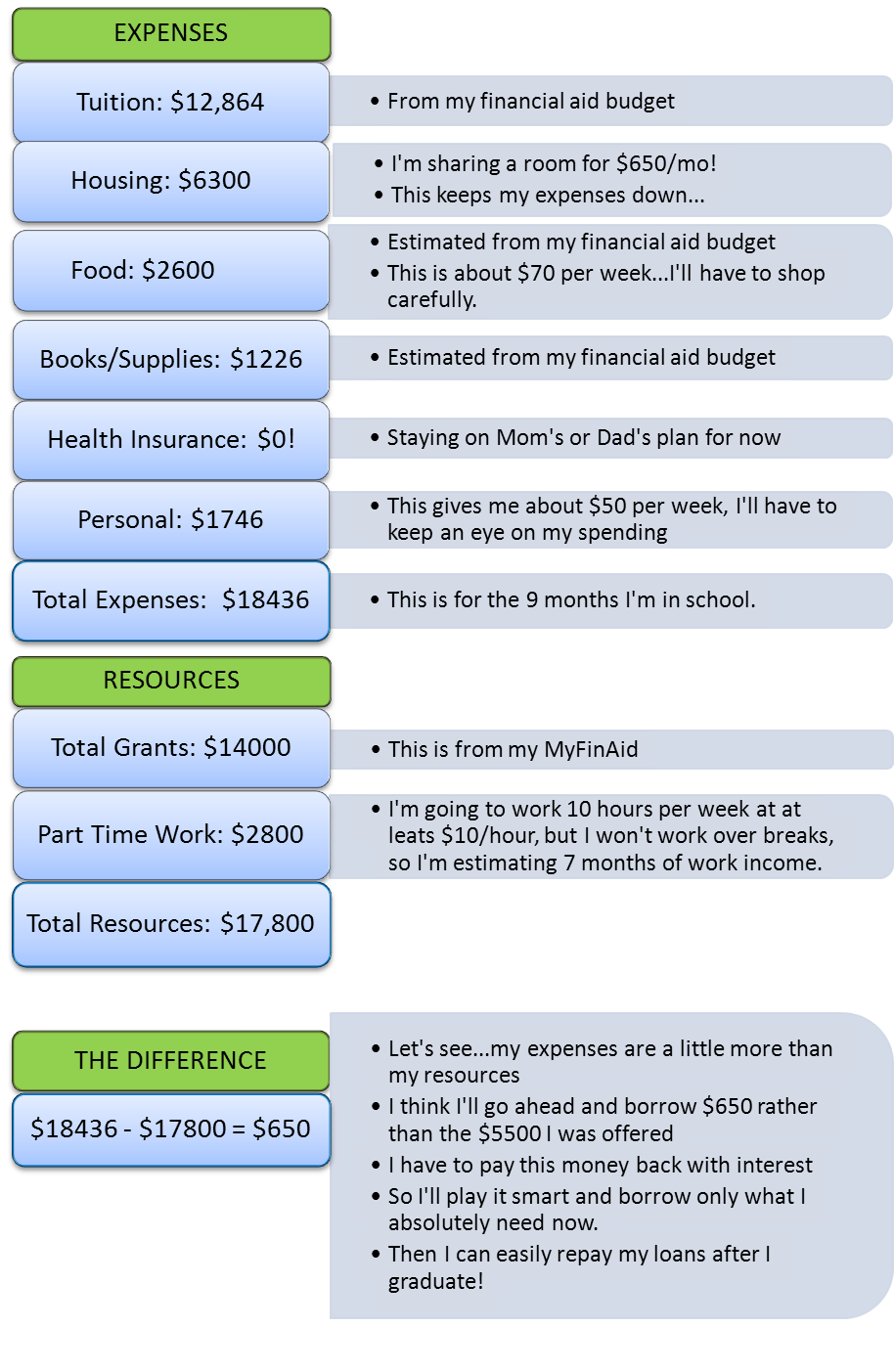

Did you know you can borrow less than your total loan offer?

A little math now can save you hundreds or thousands of dollars later! Wise borrowing means knowing how to figure out how much you need to borrow to cover your expenses and borrowing only that amount. Take a look at this budget example to help you think about your own budgeting process.

This loan is available to undergraduate students who meet basic eligibility requirements.

The U.S. Department of Education pays the interest on a Direct Subsidized Loan:

While you’re in school at least half-time

For the first six months after you leave school (referred to as a grace period)*

During a period of deferment (a postponement of loan payments)

*Note: If you received a Direct Subsidized Loan that was first disbursed between July 1, 2012, and July 1, 2014, you will be responsible for paying any interest that accrues during your grace period. If you choose not to pay the interest that accrues during your grace period, the interest will be added to your principal balance.

See more information about eligibility requirements, interest and fees, repayment option and the latest federal student aid updates.

The Department of Education has information about eligibility, borrowing limits, interest and fees, repayment information, and the latest federal student aid updates.

Helpful Tips

After you receive your official financial aid offer, you can work on completing loan requirements. To begin, you should:

Review this student loan checklist for required online processes that you need to complete in order to receive your loan funds.

Your interest rate is determined by the first disbursement date of your loan and your academic level. You can view the latest and previous interest rate information here.

Your maximum annual and aggregate borrowing limit depends on your undergraduate grade level and your federally determined dependency status, or your graduate student status. Loan amounts for one-term graduating seniors are pro-rated based on the number of units of enrollment for the term.

Note that if you advance from freshman class level to sophomore class level during the academic year, or from sophomore class level to junior class level, you become eligible for increased annual limits. If you wish to have your loan eligibility re-evaluated based on a class level change during the academic year, please contact Cal Student Central.

Remember that you can borrow less than the maximum amount each year. Doing so will help keep your total debt low.

Your maximum annual and aggregate borrowing limit depends on your undergraduate grade level and your federally determined dependency status, or your graduate student status. Loan amounts for one-term graduating seniors are pro-rated based on the number of units of enrollment for the term.

Note that if you advance from freshman class level to sophomore class level during the academic year, or from sophomore class level to junior class level, you become eligible for increased annual limits. If you wish to have your loan eligibility re-evaluted based on a class level change during the academic year, please contact Cal Student Central.

Remember that you can borrow less than the maximum amount each year. Doing so will help keep your total debt low.

Once you’ve decided to borrow a federal student loan, you’ll need to complete some online processes before the loan can pay (disburse). You can also print a Federal Loan Checklist for Students to help you keep track of your application progress.

To receive a Federal Direct Loan at UC Berkeley, you need to complete required processes by the following deadlines at the latest:

After 2 to 3 business days, your Master Promissory Note and Entrance Loan Counseling will be received by the Financial Aid and Scholarships Office.

After verifying that you do not have any blocks, that your financial aid application is complete, and that you meet all other basic eligibility requirements, your loan will disburse to your account.

WHERE DOES YOUR LOAN GO?

Your loan disburses to your student account and pays for any outstanding charges that you have for the term that the loan is disbursed.

If there is no outstanding balance on your student account when the loan is paid, or if your loan disbursement is larger than your balance, you will receive a refund.

If you are going to receive a refund, you will get a notification from Billing and Payment Services.

Within 120 Days of Disbursement

You can cancel or reduce a paid loan through a request to the school for up to 120 days from the original disbursement date. It is important to remember that a reduction or cancellation of a paid student loan will create a charge on your student’s account that must be paid within no more than 30 days.

If you reduce your loan using these directions, send your payment to UC Berkeley once you see the charge on the student account.

To reduce or cancel a federal student loan, the student should open a case with the requested change.

Note: When you cancel your loan through the school by reducing the amount, a charge will be applied to your student account within 2 to 3 business days, which may create a balance due. You are responsible for paying this balance.

Do not send a payment to your loan servicer if you are reducing the loan through the school.

More Than 120 Days After Disbursement

If it has been more than 120 days since your loan disbursement date, you cannot cancel or reduce your loan through the school. However, you can make a payment directly to your servicer. Locate the servicer’s contact information by going to https://studentaid.gov/h/manage-loans and clicking on the “View My Account” button to view your federal student loans.

In order to ensure that your payment is applied to a particular loan, you must include a letter to the loan servicer with your payment that has specific instructions about how to apply your payment.

For example: “Please apply this $200 payment to my unsubsidized loan first disbursed on 01/10/2019, paying off any accrued interest and then applying any remaining payment to the principal of that loan.”

{kind=link}